The new provisions of Tax Collection at Source (TCS) kicked in from 1st October 2020. In conversation with ChiniMandi News, Mr. Kinjal Shah a practicing CA with two decades of experience in Financial and Capital markets and speciality in Securities law, IT Security audit and Forensic audit shared his and his team member – Vatsal Paun’s views on TCS.

Excerpts:

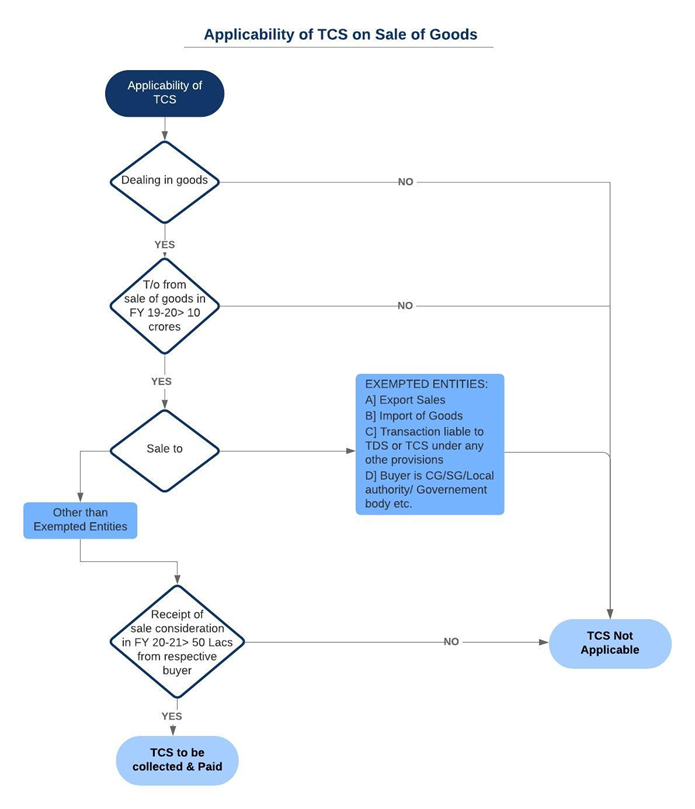

What is TCS (Tax Collection at Source)?

TCS is collection of Tax at Source by seller from buyer. If the seller has sold goods worth Rs. 1 Crore and applicable TCS rate is 1% then the Seller will collect Rs. 1.01 Crore from buyer and pay Rs. 1 Lac to government so collected from buyer with relevant details of buyer.

What is the difference between TCS and TDS?

TCS liability is on the seller or the person who collects the payment whereas TDS liability is on the payer.

What are new provisions relating to TCS?

With effect from 1st October 2020 TCS provision has been made applicable subject to certain conditions for the following:

- Foreign Remittance under Liberalised Remittance Scheme (LRS) – [Sec. 206C(1G)(a)]

- Educational loan taken U/s 80E and remitted out of India – [Sec. 206C(1G)(a)]

- Sale of overseas tour package – [Sec. 206C(1G)(b)]

- Sale of any goods – [Sec. 206C(1H)]

Note: TCS is applicable on point (1) & (2) above only if the amount in a financial year exceeds Rs. 7 Lacs whereas for point (3) TCS is applicable without any threshold.

In order to decide on the applicability of this provision, turnover of which year must be considered to determine its applicability?

For current FY 2020-2021, turnover of the preceding financial year i.e. FY 2019-20 must be considered.

If turnover in FY 2019-20 exceeds Rs. 10 Crores, provisions of TCS shall become applicable.

From whom to collect TCS?

TCS is to be collected from all buyers to whom goods are sold except in respect of sales to –

- Central Government, a State Government, an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State; or

- A local authority [Refer: Explanation to clause (20) of section 10] or

- In respect of export sales or in respect of person importing goods in India

- Any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein.

- In respect of transaction on which TDS or TCS under any other section of Income Tax Act is applicable

Are there any threshold limits for TCS?

- TCS is applicable on receipts of sales consideration exceeding Rs.50 Lacs from a single buyer in one financial year.

- Receipt of sales consideration includes sales of previous years realised during the current financial year. TCS is not required to be collected and paid in respect of first Rs.50 Lacs from each buyer.

When to Collect TCS amount?

TCS is to be collected at the time of any receipt of payment for the above sale.

Should TCS be collected in the invoice or at the time of receipt of sales consideration?

The provision uses the words “receives any amount as consideration for sale of any goods” indicating that TCS is required to be collected and paid only against receipt of sales consideration.

Whether TCS to be collected on receipt of Advance?

Yes, CBDT has clarified vide circular No. 17 of 2020 dated 29th September, 2020, that TCS to be collected at the time of receipt of payment and hence in case of receipt of advance amount towards sale, TCS is to be collected on such advance.

Any adjustment to be made for discount or goods return?

No, CBDT has clarified vide circular No. 17 of 2020 dated 29th September, 2020, that no adjustment to be made in case of discount and goods return as TCS is to be collected at the time of receipt of payment and on the amount so received.

Should TCS be collected on Taxable value or on Gross Total Value including GST and other charges?

Yes, the consideration will include GST and other charges for collection of TCS. Section 206C(1H) provides that the seller should collect from the buyer, TCS on any amount received as consideration for sale of goods. Since the words used in the said provisions is “any amount received towards the sale consideration” TCS must be collected on Gross Total Value including all additional charges and GST.

Further, CBDT vide circular No. 17 of 2020 dated 29th September, 2020 has clarified that the consideration will include GST for collection of TCS

What will be the applicable rate of TCS?

Applicable TCS rate on amount of consideration received exceeding of Rs.50 Lacs:

| Pan/Aadhaar available | Pan/Aadhaar not available | |

| Up to March 21 | 0.075% | 0.75% |

| From April 21 | 0.1% | 1% |

When TCS Payment will be made to the Government Treasury and what about filing TCS Returns?

Payment of TCS collected is required to be made to the government within 7 days of the next month in which the amount is collected.

Return of the TCS would be filed in Form 27EQ on or before the 15th day of the month succeeding to the quarter except for the last quarter where the due date would be 15th May.

In the case of Works Contract, whether the contract value will be required to be segregated into Goods & Services and TCS will be required to be collected on Value of Goods Only or Full Value of Works Contract?

Since works contracts are subjected to TDS provisions u/s 194C, provisions of TCS u/s 206C(1H) shall not apply and no segregation between value of goods or services will be required.

Whether sales made to public sector companies substantially or wholly owned by the Central or State government will be outside the purview of these provisions?

No. Since exemptions from TCS provisions are specified only for Central & State govt, receipt of sales considerations from all other companies including centre or state owned companies will be covered within the said TCS provisions.

In case of decentralized accounts by a company having operations from multiple locations or multiple states, a limit of Rs. 50 Lacs should be determined location wise or in aggregate?

TCS provisions of sections 206C(1H) must be applied in aggregate. To overcome this difficulty, the companies will have to devise a system to identify such customers and report the same accordingly.

Whether the goods must be exported by the assessee himself or can exports by Merchant exporters shall also be eligible to qualify as exports.

The provision uses the words “other than the goods being exported out of India” to exempt assessee from the said provision. There is no specific requirement or condition for the assessee to export goods himself.

Hence, in our view, sale to Merchant exporters should qualify as “for the purpose of exports” if necessary declarations and undertaking are available with the seller.

Whether credit for TCS paid will be allowed?

TCS is similar to your advance tax or TDS and hence, credit for the same shall be allowed from your final tax liability.

Also you must take your TCS credit into consideration while computing your advance tax liability.

Illustration

Below are the various illustrations in respect of each buyer to understand the applicability of the provision:

| Sales from 1.4.20 to 30.9.20 | Sales from 1.10.20 to 31.3.21 | Amount received from 1.4.20 to 30.9.20 | Amount received from 1.10.20 to 31.3.21 | Receipt of sale consideration in FY 20-21 in excess of Rs. 50 Lacs | TCS to be collected on amount |

| [1] | [2] | [3] | [4] | [5]=[3]+[4] – 50 Lacs | [6]=[4] or[5] whichever is lower |

| 60 Lacs | Nil | 60 Lacs | Nil | 10 Lacs | Nil |

| 70 Lacs | Nil | 40 Lacs | 30 Lacs | 20 Lacs | 20 Lacs |

| 70 Lacs | Nil | 60 Lacs | 10 Lacs | 20 Lacs | 10 Lacs |

| 20 Lacs | 50 Lacs | 70 Lacs** | Nil | 20 Lacs | Nil |

| 70 Lacs | 40 Lacs | 60 Lacs | 30 Lacs | 40 Lacs | 30 Lacs |

| Nil | Nil | 40 Lacs*** | 20 Lacs*** | 10 Lacs | 10 Lacs |

| 100 Lacs | 20 Lacs | Nil | 120 Lacs | 70 Lacs | 70 Lacs |

| Nil | Nil | 40 Lacs** | 70 Lacs** | 60 Lacs | 60 Lacs |

In the above table, sales figures represents sales effected to single buyer (including GST amount) against one or many invoices.

** Receipt of Advance amount

*** Represents amount received out of sales effected in FY 2019-20.

Summary of TCS [Sec. 206C (1H)]

|

Nature of Transaction |

Threshold Limit |

Rate of TCS (%) |

Exempt Category |

Time of Deduction |

| Sale of any goods except as mentioned below:

a) Goods for Export purpose; b) Goods specified u/s 206C(1) i.e. scrap, Tendu leaves etc; c) Goods specified u/s 206C(1F) or (1G) |

a) Aggregate Value of consideration from sale of goods to respective buyer exceeds Rs 50 Lacs during the year. &b) Total Turnover of Seller exceeds Rs 10 crore in the immediately preceding financial year | a) 1% of amount received in excess of Rs. 50 Lacs, if no PAN / Aadhaar Card is received from the buyer

b) 0.075%of amount received in excess of Rs. 50 Lacs, in all other cases.

|

a) If buyer has already deducted TDS on such transaction under other provision of Act.

b)If buyer is CG*, SG**or local Authority or government body c) A person importing goods into India. |

At the time of receipt of payment of sales consideration. |

To Listen to this News click on the play button.