The coronavirus pandemic is incessantly transforming growth of several industries, however the impact in a few industries is not varied and seems hazy. While some industries have a scenario of demand booming and promising futuristic opportunities, on the other hand there is a scenario in which some industries have registered a drop in demand massively. The sugar industry has been in a nailbiter situation to witness how the world balance sheet takes shape and how the major players move ahead.

In conversation with ChiniMandi News, Mr. Ben Seed – Analyst at Czarnikow Group Limited, a leading supply chain services company shared his views on various aspects related to the supply of sugar.

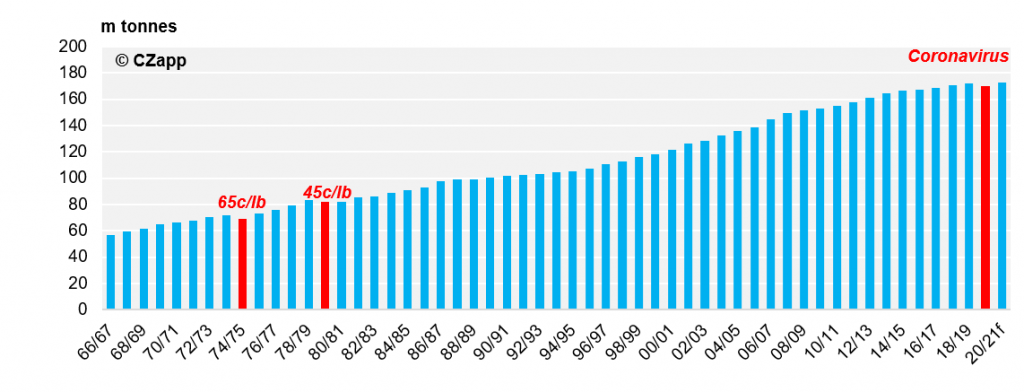

On the effect of global sugar consumption he said, “Consumption will fall by nearly 2m tonnes (1%) this year compared to 2019, due to coronavirus lockdowns.

Global Sugar Consumption

Consumption will not recover fully until life can return to normal in affected countries; at the moment this looks like being in 2021 at the earliest. This is the first time we’ve seen a year-on-year sugar consumption decline since 1980, when raw sugar prices hit 45c/lb. We believe the decrease of out-of-home sugar consumption (in bars, restaurants, theatres, etc.) during lockdowns will be larger than the increase of in-home sugar consumption. Soft drink sales have been particularly affected by the abrupt end to social gatherings outside the home.

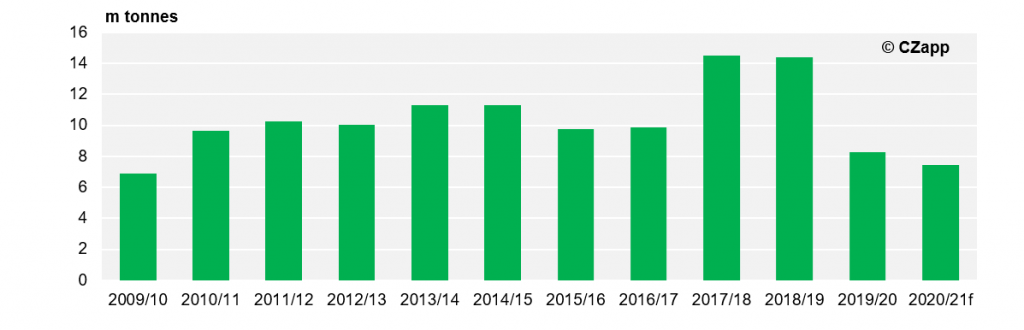

Sharing his views on white premium he said, “The refined sugar market continues to suffer from a shortfall in supply following this year’s poor Thai cane crop. This has ensured the Q/N and V/V white premiums have remained strong until recent days. We don’t expect a big increase in Thai sugar production in 2021 so white premiums are unlikely to fall back to 2019 levels any time soon.

Thailand Sugar Production

But in the medium term, we think it’s possible the white premiums could weaken a little more once it is clearer how much sugar consumption has been lost to coronavirus.

The trade flows this year will be driven by Brazil. It looks like Brazilian mills will maximise sugar production (at the expense of ethanol). Unless this changes there is too much raw sugar in the world in 2020.”

Ben also expressed his views on where he sees the world sugar sector going with emphasis on Brazil’s production. He said, “Centre-South Brazilian cane acreage has been almost unchanged in recent years because sugar and ethanol prices haven’t been high enough to justify new investments.

This means the Brazilian cane crush has been static at around 600m tonnes. Mills in CS Brazil can choose whether to prioritise sugar or ethanol depending on price. Whilst Brazil is likely to maximise sugar production this year, in future years there is no guarantee this will continue. Ethanol prices in Brazil have already started recovering so the situation could be very different even by next season.

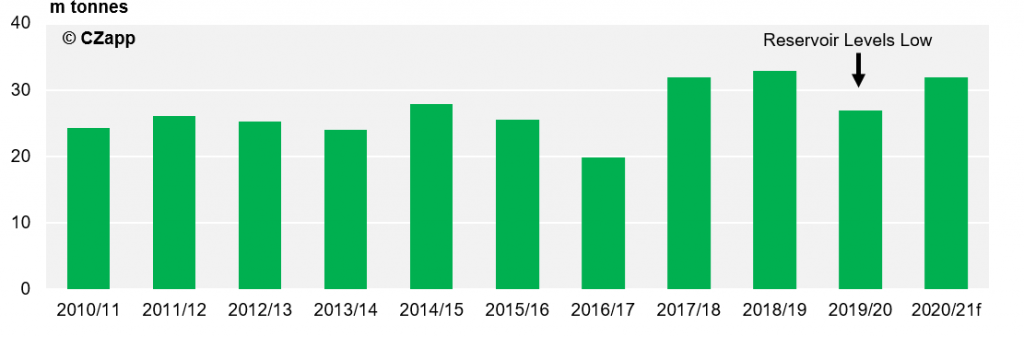

It looks like India is set to regularly produce 30m tonnes of sugar or more (dependent on the monsoon rains) which would mean that India could be the largest sugar producer in the 21/22 season. India will also therefore continue to export sugar in the coming years unless domestic ethanol production can grow rapidly.”

Indian Production

Above information is available on Czarnikow’s portal Czapp

To Listen to this News click on the play button.