With global sugar prices witnessing a sharp rally for the last few days in the wake of various factors. The industry stakeholders are anxious on how the market will react and how we stay ahead of the curve and what the future holds for the industry in this new environment.

In conversation with ChiniMandi News, Ms. Luciana Torrezan, Global Head of Sugar and Cane Ethanol Research, Tropical Research Services shared her views on the global sugar scenario.

Speaking on how she sees the global sugar market considering the factors like delay in the announcement on export policy from India, the La Nina in South America etc. she said, “Our global sugar S&D and trade flow balance-sheets are projecting a comfortable scenario for sugar supply as-at the end of the 2020-21 marketing year. Despite a delay in the announcement of India export policy, there is a consensus that some kind of support will be announced by the Government of India. Therefore, we are assuming that India exports will be able to reach the world sugar market as soon as Q1 2021. The drier-than-normal weather brought by La Nina in South America and recent hurricanes in Central America represent a small downside risk to global sugar production in the 2020-21 marketing year, but we believe that Brazil will be able to meet any shortfall through a continuing strong allocation of the “mix” towards sugar in the 2021-22 national crop year.

In this scenario, the recent rally in front month ICE New York No.11 raw sugar contract is not consistent with our base case scenario for the global sugar trade-flow balance-sheet, on a fundamental basis.”

Commenting on how the international sugar prices and trend may be in the coming days, “While there is no definition of India sugar policy, we believe speculative buyers may continue to add to their net length. Without robust selling from origin (which we do not expect until India domestic sugar export sales connect), speculative buying has the scope to produce “disproportionate” gains in ICE New York. No.11 raw sugar prices, especially if the global-macro “everything rally” continues.”

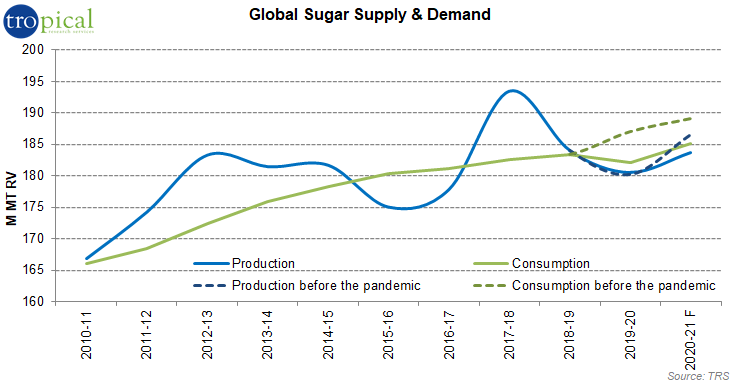

On being asked, how has Covid-19 changed the sugar market outlook, where we stand now in terms of global surplus / deficit and how have the global movements have changed, Torrezan answered, “Comparing our grids before and after the impact of the pandemic, we find that COVID affected our balance-sheets on both the supply and the demand side. Before the pandemic, we expected a quite significant global sugar deficit balance-sheet on an S&D basis. On the supply side, a sharp decline in Brazil domestic fuel prices and fuel demand – resulting from the lockdown – lead CS Brazil producers to allocate more of their production to sugar as opposed to ethanol, than would otherwise have been the case. This increase in CS Brazil sugar supply offset the sharp losses observed in Europe sugar production estimate. Estimates of global sugar demand also took a hit, particularly in Asia, Europe and the Americas, resolving the global sugar deficit on an S&D basis which we were, previously, projecting. Some of that reduction in global sugar demand has since been added back to the balance-sheet, as imports into some countries, principally China, have exceeded expectations. But our estimate of global sugar demand overall remains -8.8M MT down for 2019-20 and 2020-21 marketing years combined, relative to our pre-COVID estimates.

Our revised estimate of the global sugar S&D balance-sheet for the 2019-20 marketing year is for a -1.6M MT RV deficit, which is a -5.1M MT RV smaller deficit than the -6.7M MT RV “pre-COVID” deficit which we forecast at the time of our “Statistical Update” published in February 2020. Looking ahead, we estimate a global sugar S&D deficit for the Oct-Sep 2020-21 sugar marketing year of just -300K MT RV.”

Sharing thoughts on whether Brazil will be heading for another maximum sugar crop in April 2021, she said, “Yes. The current global sugar S&D scenario indicates that the function of the market is to generate an almost “maxi-sugar” allocation of the sugarcane “mix” in the 2021-22 CS Brazil crop year, since the world market is reliant on CS Brazil for sugar supply.”

About Tropical Research Services (“TRS”)

Tropical Research Services (“TRS”) collects, collates and analyses, research and data as to a variety of tropical commodity products, including coffee, cocoa, sugar, cane ethanol, tropical oils and tropical grains and oilseeds. TRS generates a significant information advantage as to the outlook for the forward supply and demand of tropical commodity products; a valuable resource for those deploying portfolio management and hedging and procurement strategies, in the otherwise opaque world of tropical commodity products information.