Among the myriad industries affected by the COVID-19 pandemic, sugar is one particularly critical to global markets. Many other factors have gravitated the impact.

In conversation with ChiniMandi News, an eminent international sugar analyst and broker Julian Price shared his views on the impacts of Covid-19 and climate change in trade flows and logistics. Sharing his views on how the long term effects of Covid could be hugely profound for our sugar sector, or will there be a little profound effect at all; He said, “Eventually I have alighted on the thought that we will innovate and adapt and that it will be “business as unusual”. That’s not to say that Covid-19 hasn’t been an immense, and in many cases, a tragic shock. But as far as sugar trade flows and logistics are concerned, we have, as is key in most human endeavours, adapted, innovated and learnt to live with the slings and arrows of outrageous fortune.

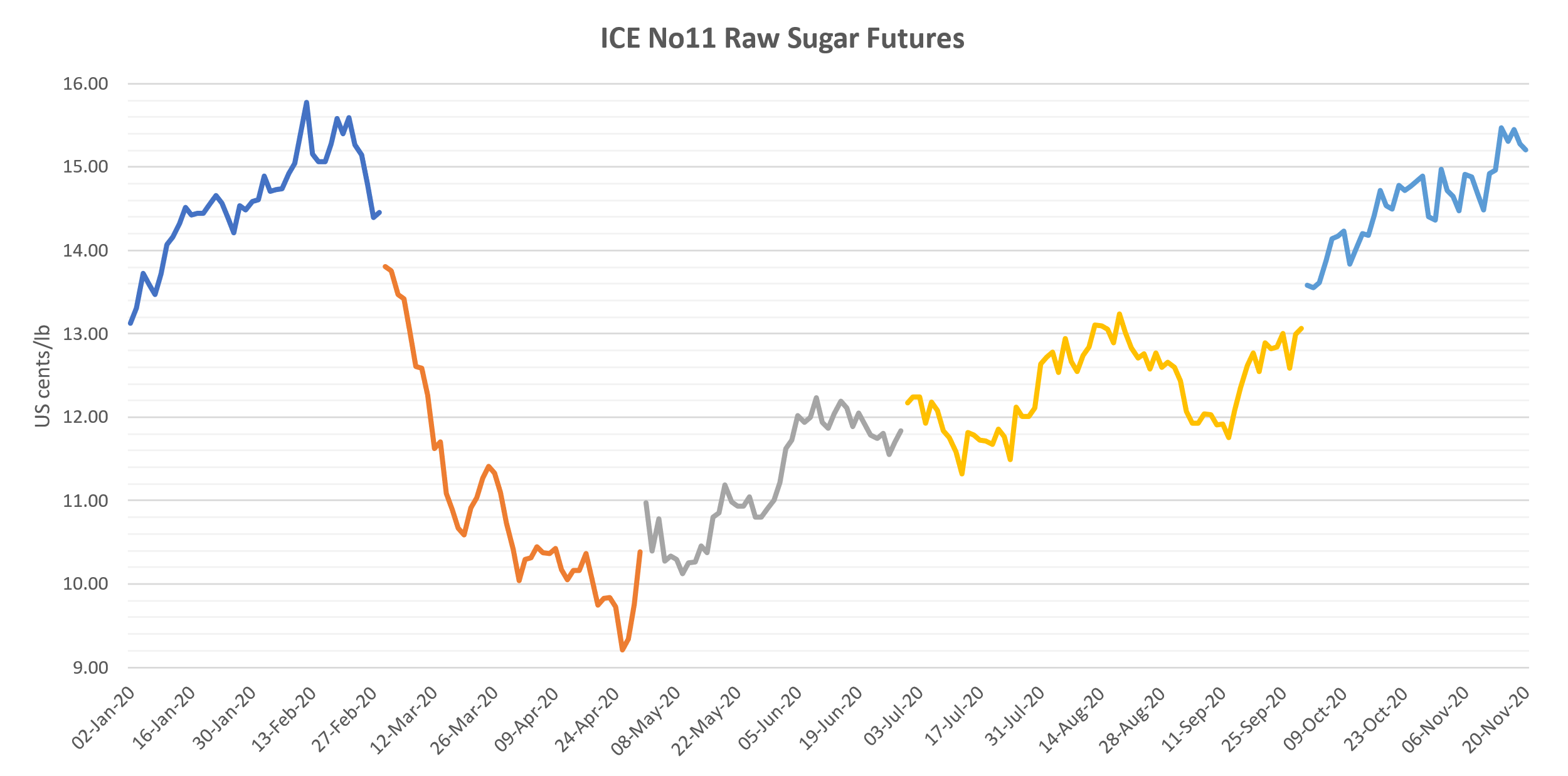

Having largely learnt to live with Covid-19, we have seen a ‘V’ shape recovery in ICE #11 sugar futures prices, however, the market structure has moved from contango to backwardation.

We have been here before in many ways. We have survived the outrageous ponzi schemes of collateralized debt obligations, the collapse of Lehman Brothers and much else besides.

Covid-19 is not yet over – maybe it will never go away – but our fear of the unknown, which perhaps can be measured by the Cboe VIX index ©, will dissipate. And by innovating and adapting we can build the resilience we will need to cope with the next crisis when it comes.

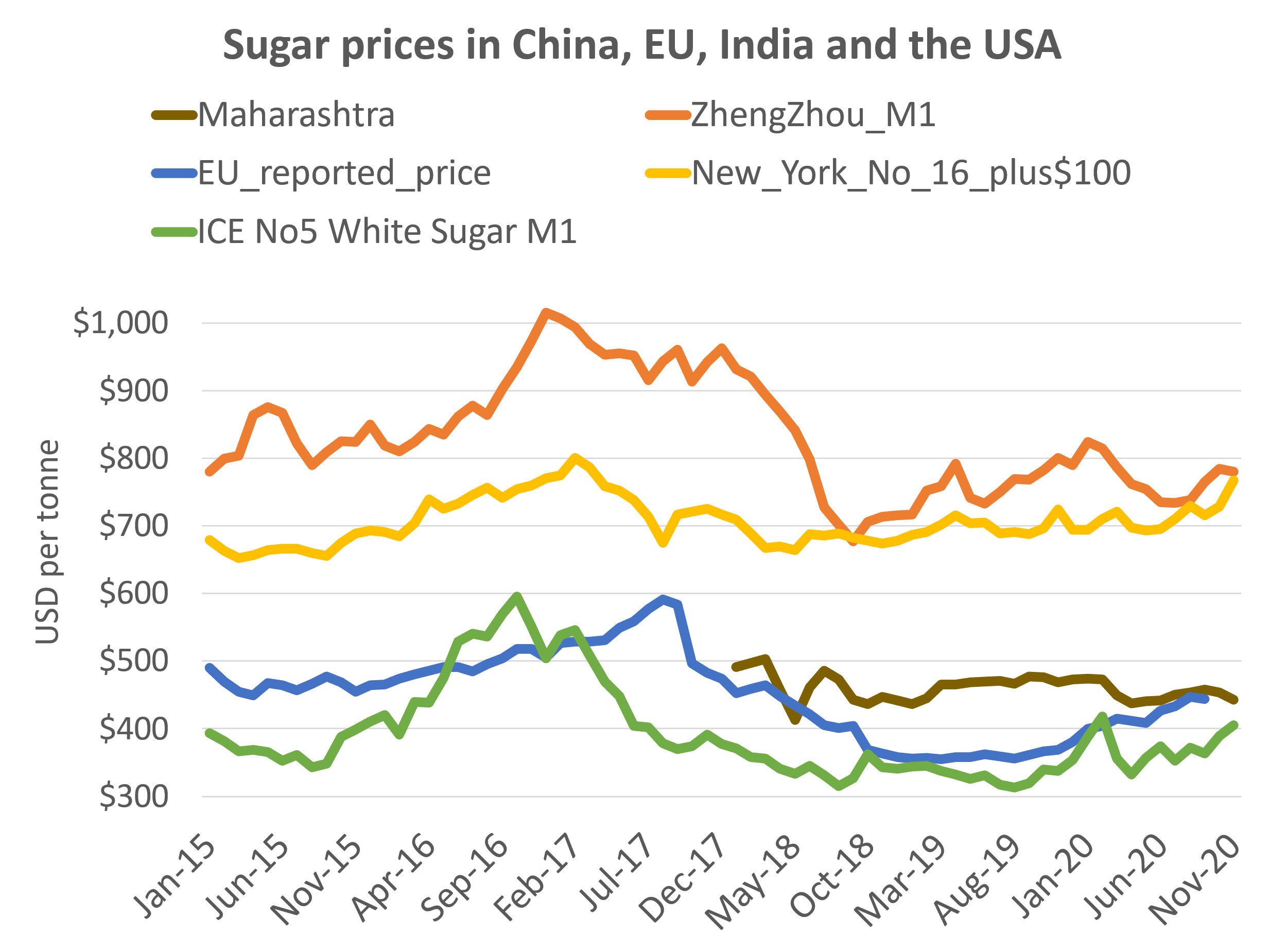

Commenting on the domestic prices of major players in the global sugar market, he said, “Closer to home, domestic sugar prices seem so far not to have been affected by this pandemic. Looking only at domestic sugar prices in China, the EU, India and the USA you would be hard pressed to discern any effect of Covid-19. Such movement in domestic prices as one can see may be attributed to normal, non-Covid reasons for example speculation of import licences in China, or anticipation of export subsidies in India.

In the case of EU domestic sugar prices, which I follow most closely, these seem at last to be showing signs of life owing to a non-Covid, non-climate, non-scientific and lamentable failure of statecraft. I refer, of course to the frankly stupid decision to ban the use of neonicotinoids to treat seed pellets in several member states, most prominently in France.

In the case of EU domestic sugar prices, which I follow most closely, these seem at last to be showing signs of life owing to a non-Covid, non-climate, non-scientific and lamentable failure of statecraft. I refer, of course to the frankly stupid decision to ban the use of neonicotinoids to treat seed pellets in several member states, most prominently in France.

Sharing his views on the impact of climate, Julian said, “Climate change too has shifted trade flows, notably caused by the drought affected crops of Thailand and elsewhere and the better rains in East & Southern Africa and Mexico and in Australia. The devastating hurricanes Eta and Iota in the Central America area are a big worry.

Non-Covid, non-climate factors have shifted trade flows and the domestic price differentials that drive these flows. Of course, India and the EU have been affected by political decisions (or their absence) and I worry deeply that war is brewing in Ethiopia, the cradle of humankind.

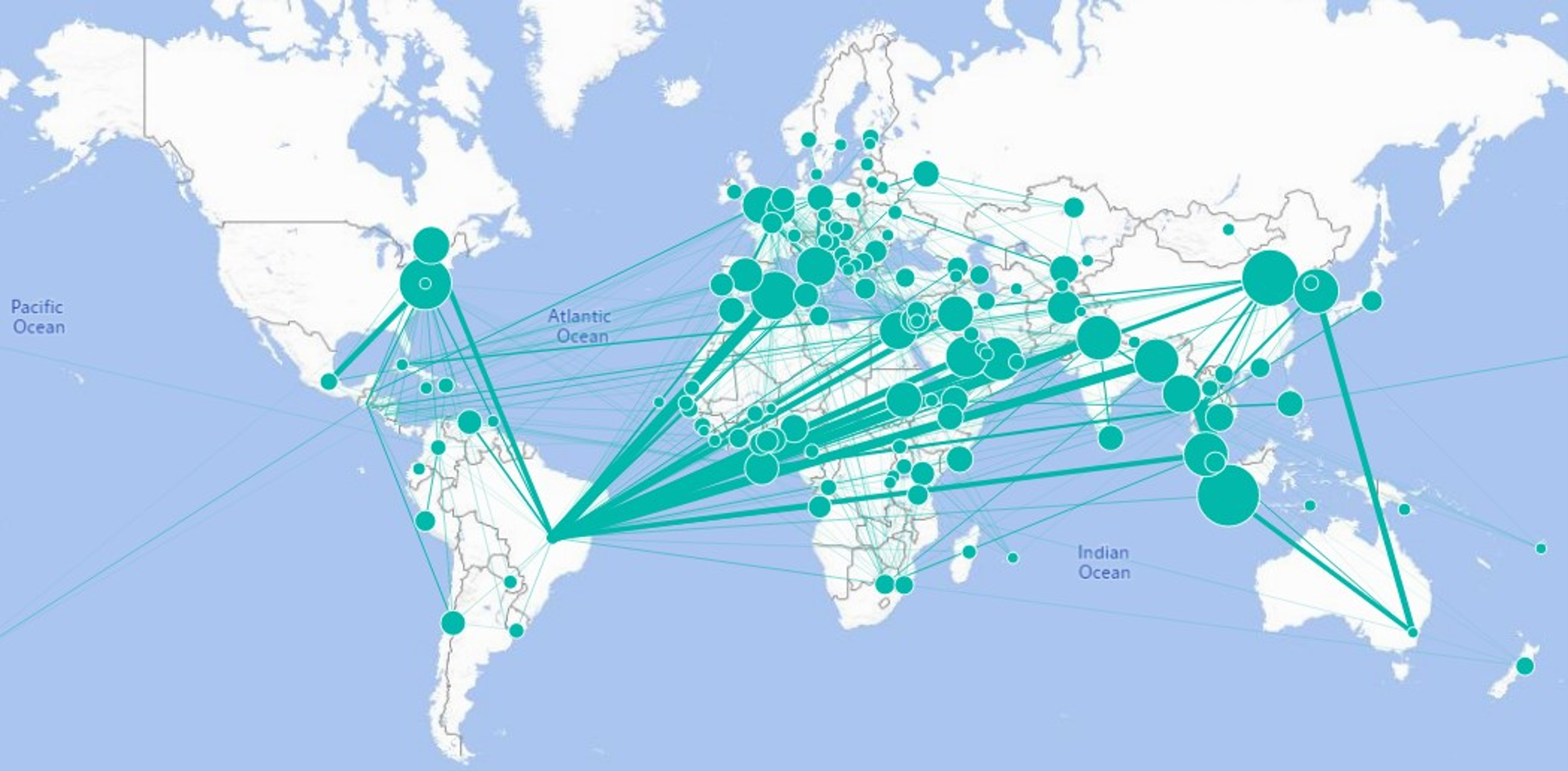

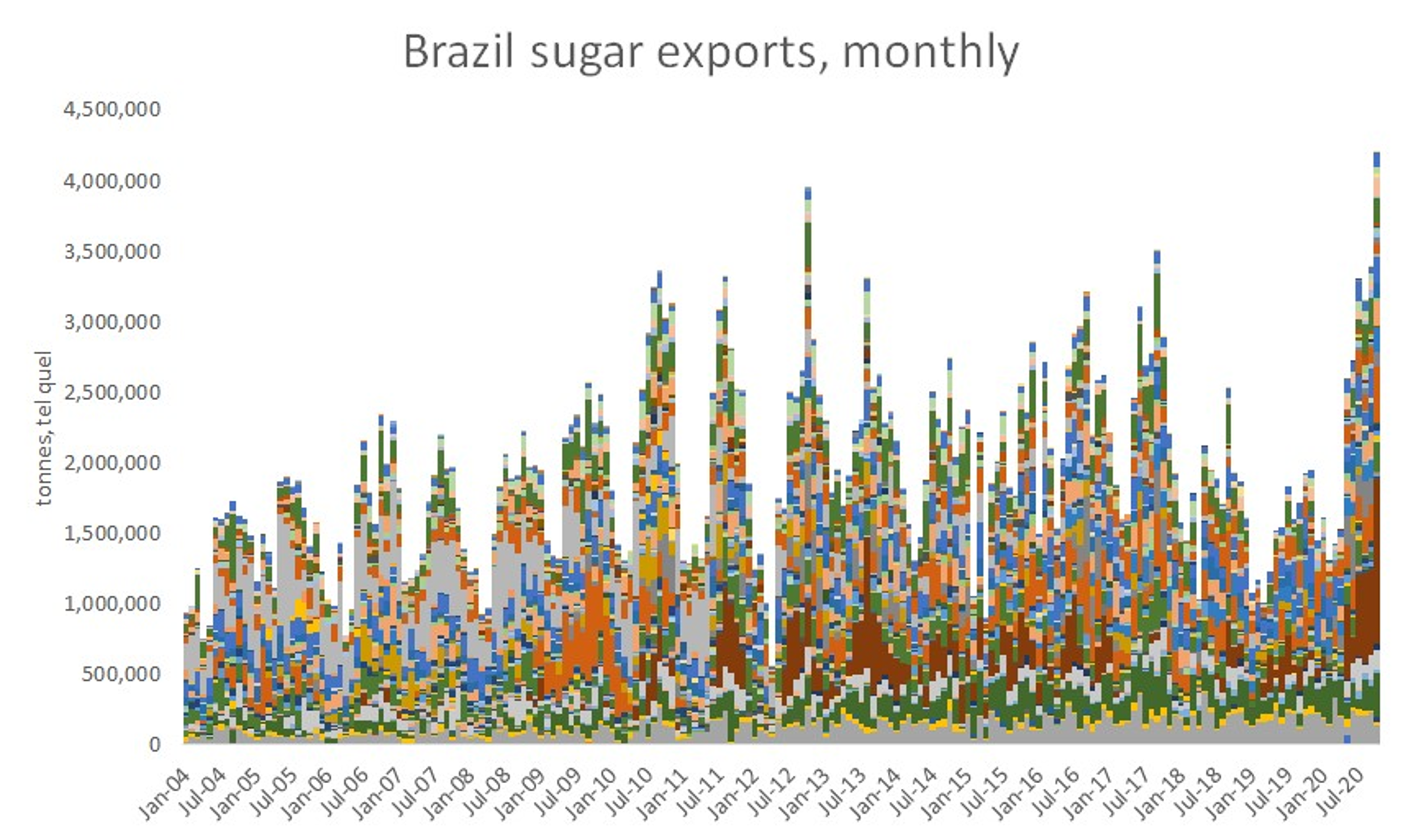

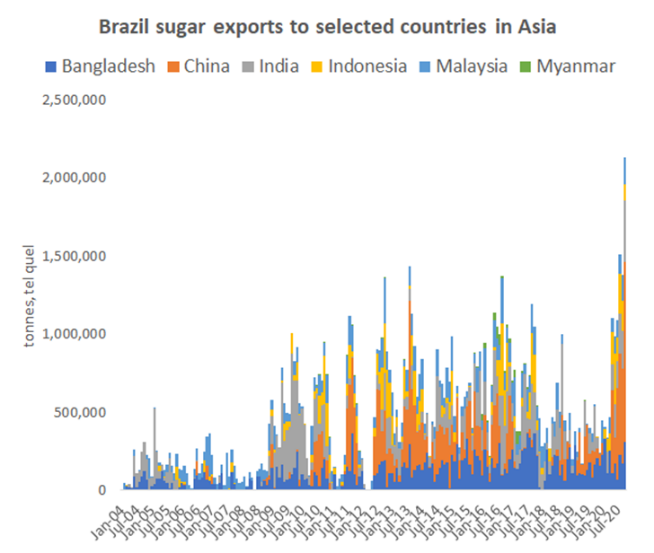

All these factors – Covid, Climate, Politics and fear – have been responsible in one way or another for the big trade flow story as this year – that of Brazil to the Far East, replacing Thai sugar in Far East demand.

As well as the increased flow of the Brazilian exports to Bangladesh, China, India, Indonesia, Malaysia and Burma, I should have added Vietnam to the graph below.

This flow of sugar from Brazil to the Far East was badly needed to solve the tightness in quarterly trade flows that had been anticipated before the Covid-19 pandemic shock. And peering into the next couple of quarters, it seems clear that Indian exports will be needed to solve the currently anticipated tightness into calendar Q1 and Q2. Moreover it seems that a decision concerning Indian exports cannot be delayed for much longer for fear of fall in local prices in India. The game theoretic term for this is called ‘chicken.’ ”

Answering a question on the effect of Covid-19 on consumption, he said “Turning to the Covid effects on consumption and therefore on trade flows, with the invaluable benefit of hindsight it would seem inescapable that some of the dire initial forecasts of demand destruction caused by Covid were a bit hasty.

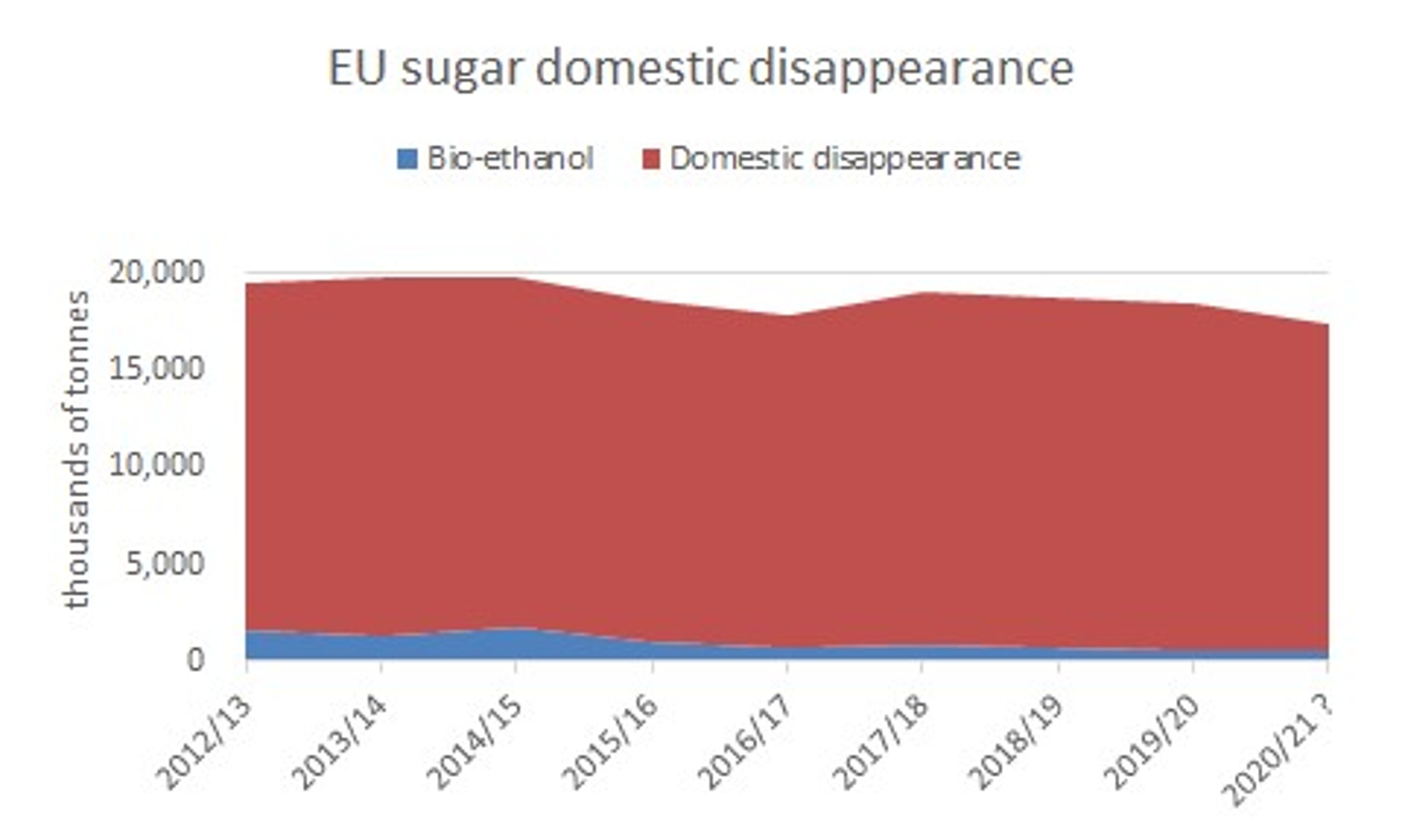

In as much as it may be possible to estimate sugar consumption, it seems that there has been a definite shift from consumption in hotels, restaurants and catering businesses which have been cruelly closed down by Covid towards consumption at home, often supplied through supermarket chains. We might also note that where sugar consumption may have been encouraged by the low prices we saw during this summer. In Indonesia we have seen industrial demand fall, home cooking rise and consumption fall overall. In China, stock surveys suggest no change in consumption. In India, mill sales data also suggest no change to consumption. In South Africa, Brazil, USA, consumption seems to have remained steady. In Europe domestic disappearance seems to have fallen 3 % or 4 %.

But again, as with Brazil and Indian supplies replacing Thais, there is an argument that lower consumption may have had a role in solving the perceived tightness in the global sugar markets. Given that the Brazilian mix is now set to “maximum sugar”, it might very well be that climate may become an even more critical factor. It is also remarkable how small, relatively, is the EU sugar beet share of ethanol.”

Julian Price also threw light on Freight & Logistics, he said “ Faced with the rapidly changing price differentials which drive global trade flows, the key bottlenecks in all of this are in the ports of loading and discharge. Sugar and other agri-food stuffs and indeed trade in goods in general – have been identified by governments worldwide as being of critical importance. Hence ports around the world, whether sea ports or dry ports or land borders have invariably remained open to trade in goods. Of course, there have been problems, for example there have been instances where ships not being granted free pratique owing to crew being tested positive for Sars-Cov-2. Moreover, the colossal deliveries of bulk raw sugar against the May and October future contracts inevitably strained operations in Santos and also in certain disports when paperwork was delayed. And also, the closure of borders to people as opposed to goods has caused problems for example for cargo supervisors. But given the unprecedented scale of the Covid shock, the remarkable resilience of port operators, the high degree of mechanization and the sheer goodwill previously earnt amongst reputable operators has shone through.

So it’s generally been business as unusual. Moreover, I believe that innovation, accelerated by Covid and manifest in changing sugar trade flows, will further build resilience in our sector.”